Back to Insights

24 June 2021

A new survey on climate change action by Lloyd’s managing agencies shows solid progress on physical risk assessment and management, but a distance to travel in other areas.

Powerful forces have made climate change a priority across the business world. In Lloyd’s, the challenge is twofold. Alongside their own climate risks, managing agencies (the insurers at Lloyd’s) take on the climate risks of other companies, especially physical risks like hurricane damage to Florida hotels. That makes climate-change risk a different beast altogether.

LMA members have achieved varied levels of progress towards embedding the management of the disconnected but correlated financial and operational climate-change risks within their businesses, according to a recent survey by Willis Towers Watson for the Lloyd’s Market Association. In short, progress on third-party physical risks has been good, but the market in general has a way to go on the rest.

Two-speed progress

Physical climate risks are getting plenty of attention, the survey found. For example, managing agents have typically made frequency and severity adjustments to their natural catastrophe modelling to take climate-change impacts into account, particularly by altering windstorm tracks and reconsidering increased losses due to flooding. Most have taken an exposure and accumulation management approach to physical climate risk management.

In contrast to this comprehensive work, the Lloyd’s market has made less progress in areas which focus on managing agencies’ own risks, including:

- Disclosure

- Operational resilience

- Asset risk

- Transition risk

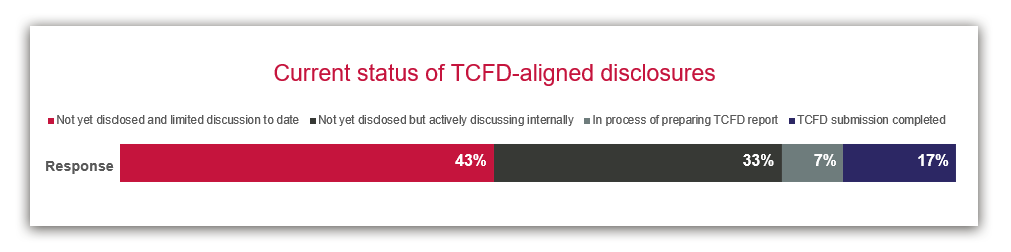

For example, only roughly one in six managing agencies has made complete ‘TCFD disclosures’ (about 17%), compared to more than three quarters that have not yet begun to prepare disclosures, including 43% that have had, at best, only limited discussions about their disclosure. Such reporting according to guidelines set by the Task Force on Climate Related Financial Disclosure (TCFD) is expected to become mandatory in 2022.

“The survey results tell us that the market would benefit from specific guidance, help with interpretation, and a collaborative perspective,” says David Singh, co-chair of the LMA Climate Risk Working Group and Exposure Management Delivery Manager at MS Amlin, who led a videoconference meeting of Managing Agents convened to present the findings.

Getting ready

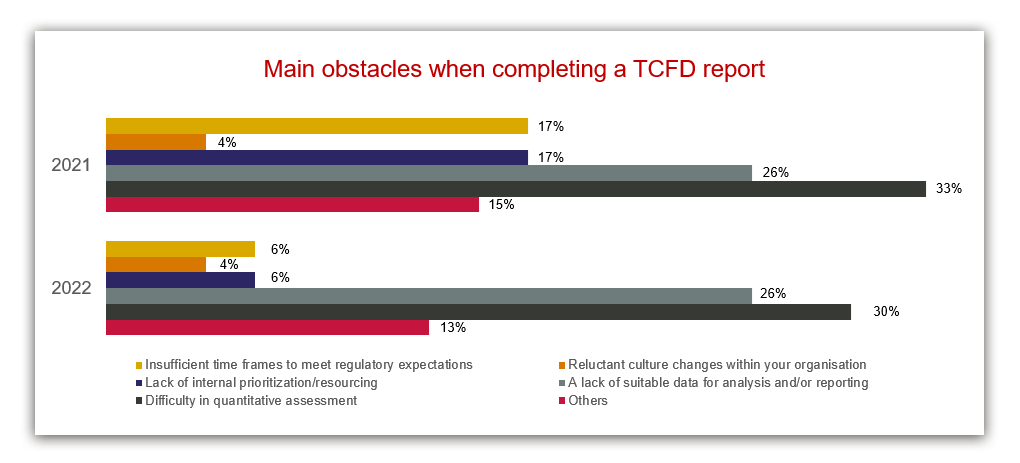

Adhiraj Maitra, the Willis Towers Watson Director who led the research, described 543 responses from individuals at 51 managing agencies as “unexpectedly great”. Yet despite the enthusiastic response, companies are running into obstacles in their climate reporting. Stretched resources may be part of the problem. “A lack of prioritisation or resourcing this year was cited by 17%,” Maitra said, noting that figure falls to 6% for 2022. “It seems that 2021 is a key year to raise awareness, to allocate resource, and to do more work around governance and structuring.”

|

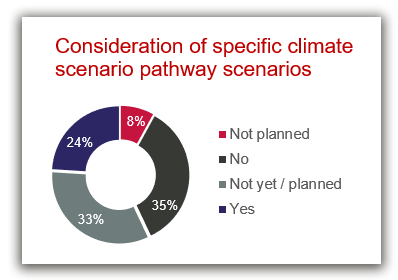

Many others blamed a lack of suitable data, or difficulty in quantitative assessment. “Everyone is struggling with suitable data across the market, and trying to find alternatives,” Maitra said. Scenario analysis could be useful in its absence, but 76% of respondents have not yet begun consideration of specific climate pathway scenarios.

Scenario modelling

The survey showed that scenario modelling is the area where responding managing agents most need support, according to Daniel Purdy, a Senior Consultant in the Willis Insurance Consulting and Technology practice. About one in five say they do not need support, “but that may be because they are not yet advanced in thinking about TCFD disclosures, and embedding it in their framework,” he surmised.

|

|

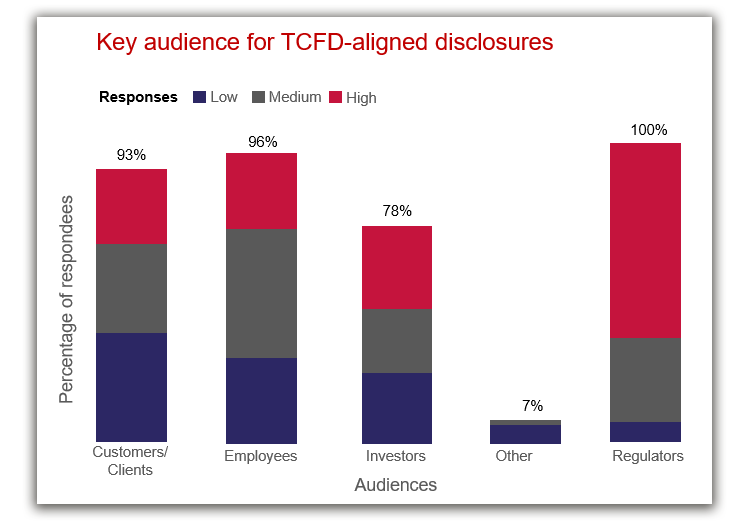

Purdy also found that managing agencies see TCFD disclosures very much as a reporting exercise. “The perception is that the regulator is the biggest and most material audience for TCFD disclosures,” he said. All respondents cited regulators as a key audience, with 69% of those stating they are high materiality. That compares to 93% citing customers and clients, of whom only 26% see them as a high materiality audience, a figure that Purdy described as “lower than we expected”.

Governance is key

Willis knows that a strong governance framework is an importance catalyst to progress, so made it a key survey topic for investigation. Maitra said governance provides the “framework to think about climate risk in a structured way.” In the area of climate-related metrics and remuneration for corporate leaders, Lloyd’s managing agencies rank behind companies polled from outside the Lloyd’s market.

Hannah Summers, Associate Director, Executive Compensation, at the firm said that a link between climate change action and executive compensation is an easy win. “An organisation’s people have a huge role to play, and arguably the HR team within these have a pivotal role in stewarding the transition to net zero,” she said. “Incentive links are an essential for some investors, and a key tangible mechanism in the transition to net zero.”

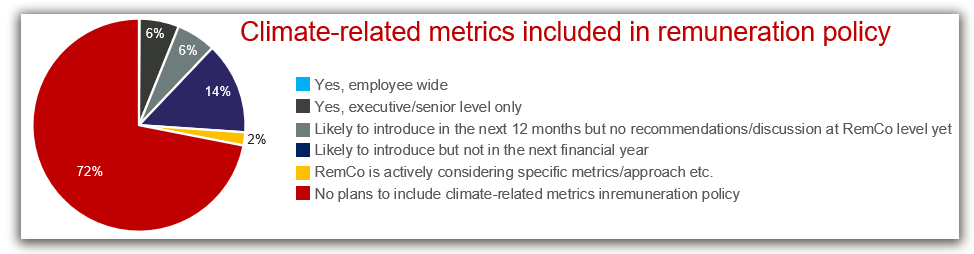

Despite this, 72% of managing agencies have no plans to include climate-related metrics in remuneration policy. Only 6% currently do so. Board-level risk committees, executive risk committees, and entire boards are the governance groups most engaged in discussions on the financial impact of climate change, followed by finance and investment committees.

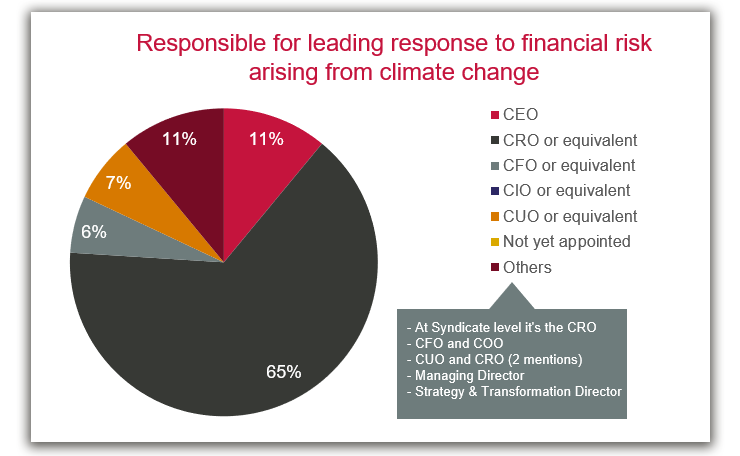

Nearly two-thirds of responding companies have assigned responsibility for the management of the financial risks and opportunities of climate change to the Chief Risk Officer, and 71% have appointed an individual or a small team to manage the firm’s climate and ESG related work. Perhaps unsurprisingly, companies with a gross premium of less than £400 million are much less likely to have made a decision about who will manage the effort.

Catch-up time

Comprehensive discussion of physical risks due to the twofold climate-change challenge faced by Lloyd’s managing agencies may be the reason they have, in some cases, fallen behind in other areas. “If you get the governance sorted first, then move on to strategy and risk management, then metrics and targets, everything should follow that natural flow,” said Zoe Nicholas, a Senior Actuarial Analyst at Willis. “If you hone in on and address the strategy and risk management areas, then your metrics and targets should catch up.”

The survey reveals that much work remains, and that the LMA has a role to play in supporting managing agencies. “Senior management has a degree of uncertainty as to what questions they should be asking, and therefore what actions they should be taking as a consequence,” said Vinay Mistry, co-chair of the LMA Climate Risk Working Group and Chief Risk Officer at Apollo Syndicate Management. “We will use this survey as a conduit to feed back to our colleagues in the Corporation of Lloyd’s to identify where we can provide help and assistance in terms of meeting the regulatory requirements on an individual basis, but also as a market.”

The LMA’s Working Group has dipped the thermometer and taken the market’s temperature, Mistry said, and learned from the effort that “clearly there’s a lot still to do.”